In this article

- The MOBI.E model: Europe's bring-your-own-power experiment

- What is MOBI.E?

- What are MOBI.E’s benefits?

- What are MOBI.E’s weaknesses?

- Switching from MOBI.E to RJME: key changes for CPOs

- Three major challenges for your MOBI.E to RJME migration

- Implications for charge point operators

- The broader context of the Portuguese charging transition

- The future of EV charging in Portugal

Portugal's electric vehicle charging market is undergoing a fundamental restructuring. After more than a decade operating under one of Europe's most distinctive market models, the country is moving away from MOBI.E and transitioning to the RJME framework. That framework more closely resembles the standard approach used across Europe.

However, this switch represents a fundamental shift in how charging infrastructure operators, energy suppliers, and drivers interact within the EV charging ecosystem in Portugal. Let us dissect the Portuguese EV charging market and its transition towards a more open model, driven by AFIR.

The MOBI.E model: Europe's bring-your-own-power experiment

The MOBI.E transition matters beyond Portugal's borders as it opens up the market for new CPOs to enter, offers lessons about the bring-your-own-power model, and highlights the critical role of back-end flexibility in navigating regulatory change.

To understand what's changing, we need to first understand what made Portugal's model distinctive.

What is MOBI.E?

Since its launch in 2015, the MOBI.E (Mobilidade Eléctrica) system operated as a centralised platform that all public charging infrastructure had to connect to. Unlike most European markets, where roaming agreements are negotiated between individual operators, Portugal mandated universal roaming through this central hub.

Any driver with a valid token could access any public charger in the country. This worked regardless of which charge point operator (CPO) owned the infrastructure or which eMobility service provider (eMSP) issued the token.

But the real complexity—and innovation—lay in how the energy economics were structured.

What are MOBI.E’s benefits?

1. Total national interoperability

MOBI.E’s greatest achievement was creating a single, integrated network. Portugal had a ‘Universal Access’ model: if you have a contract with one provider, your card or app works at every single public charger in the country.

2. Early and efficient coverage

Because MOBI.E was a government-led initiative, it prioritised coverage over immediate profit. It means that charging stations were installed in all 308 municipalities of Portugal. This approach effectively killed range anxiety early on.

3. Integrated billing and fleet management

The centralised nature of MOBI.E allowed for a clearing house for data and money. For businesses, this means all electricity used by their fleet across dozens of different charging networks is consolidated into one single invoice.

4. A lab for innovation

MOBI.E acted as a ‘testing lab’ for the rest of Europe. By having a centralised software back end, Portugal was able to test large-scale roaming and smart-grid integration long before international standards, like OCPI (Open Charge Point Interface), were fully matured.

What are MOBI.E’s weaknesses?

In most European markets, the CPO purchases electricity from the grid. They add their margin and operational costs. Then the charge point operator either sells directly to the driver (ad hoc charging for non-registered users, or through driver subscriptions directly to the CPO) or to an eMSP (who then sells to their subscribers). The energy flows through the CPO's contract.

1. Bring-your-own-power

In the MOBI.E system, the eMSP (called CEME - Comercializador Eléctrico de Mobilidade Eléctrica), not the CPO, held the responsibility for providing the energy to the driver.

This ‘bring-your-own-power’ approach meant something specific. For every charging session, the Distribution System Operator (DSO) needed to identify precisely which eMSP to invoice for that specific amount of energy consumed. The CPO's electricity bill would then be adjusted to exclude energy consumed through public charging sessions.

2. Operational complexity

Think about the administrative complexity this created. A single charge point might serve customers from 40+ different eMSPs in a month. For each transaction, the DSO needed accurate attribution data to invoice the correct party. It required sophisticated real-time data flows, accurate metering at 15-minute intervals, and careful reconciliation processes.

This created an unusual market structure with:

1. CPO wholesale costs: Infrastructure, land usage, grid connection, and operational margin.

2. eMSP retail costs: Energy procurement, user acquisition, subscription management, and margin.

The two were kept separate. MOBI.E acted as the supervising entity that coordinated authorisations and managed the data flows that the DSO needed to properly invoice each eMSP.

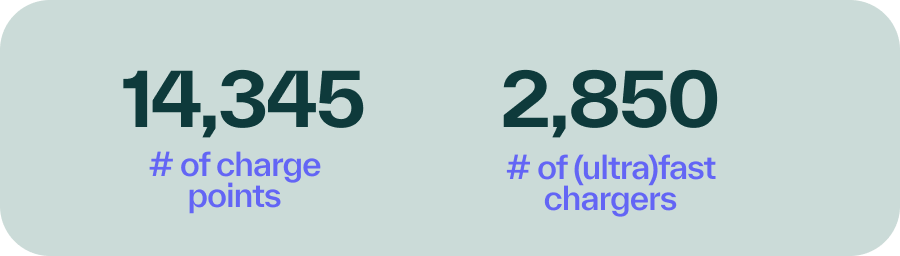

Figure 1. Number of charge points and (ultra)fast chargers in Portugal (Source: retrieved from Mobie.pt on 9 March 2026).

3. Authorisation by MOBI.E

Every charging session required real-time authorisation from MOBI.E. When a driver presented their token at a charger, the CPO's back-end system wouldn't make the authorisation decision itself. Instead, it would forward the request to MOBI.E, which would verify the token's validity and authorise the session. MOBI.E then tracked every transaction across the entire network, ensuring the proper attribution of energy consumption.

For context, Portugal has around 14,341 public charging points in March 2026. Approximately 100 registered CPOs and 40 eMSPs operate in the market. The centralised model ensured interoperability across this fragmented landscape without requiring bilateral roaming agreements between every possible combination of operators.

Interestingly, Germany is beginning to explore similar bring-your-own-power approaches through what's called the Durchleitungsmodell framework. These initiatives remain in early pilot stages with only a handful of locations operational as of late 2025.

Switching from MOBI.E to RJME: key changes for CPOs

In August 2025, Portugal's new Legal Framework for Electric Mobility (Regime Jurídico da Mobilidade Elétrica, or RJME) entered into force. The Portuguese government wanted to adapt to how the Portuguese and European markets had matured and align with European standards.

The original MOBI.E model was designed to jumpstart a nascent EV charging market. A decade later, with infrastructure more established and market dynamics better understood, the regulatory rationale for such heavy-handed central coordination has diminished.

But there's also a practical reality. The MOBI.E model created significant operational complexity.

‘The transition period from the legacy MOBI.E model to the upcoming RJME model runs until 31 December 2026. This gives operators time to adapt their systems and business models.’

The new RJME framework is fundamentally altering the market structure. All charge point operators will need to have moved to the new RJME model by the end of 31 December 2026.

Key changes for CPOs include:

1. Elimination of the mandatory intermediary role

The CEME (eMSP) is no longer a required intermediary. CPOs can now sell energy directly to drivers or work with eMSPs under standard European arrangements.

2. Transition away from MOBI.E

MOBI.E continues to exist in a supervisory capacity as EADME (Electric Mobility Data Transmission Entity). It's responsible for data transmission to Portugal's National Access Point. But connecting public charging infrastructure to its platform is no longer a reality.

3. Introduction of ad-hoc payment requirements

Chargers rated 50kW and above must now accept ad hoc (direct) payment. All public chargers must offer QR code payment options. This aligns Portugal with the EU's Alternative Fuels Infrastructure Regulation (AFIR).

4. Mandatory price transparency

The new framework requires that drivers can see pricing information before starting a charging session. Price transparency in EV charging is one of AFIR's key provisions, and one that strengthens consumer protection across European charging markets.

5. Vehicle-to-Grid (V2G) enablement

The framework introduces communication standards to support bidirectional charging. This positions Portugal for V2G adoption in line with broader European initiatives.

Three major challenges for your MOBI.E to RJME migration

At GreenFlux, we're helping EDP navigate this transition. They're one of Portugal's largest CPOs, operating over 3,400 charging points across their network. This includes partnerships with major brands like ALDI, CTT, and McDonald's.

As one of the first operators managing this migration, we have learned several critical challenges that any operator undergoing this transition will need to address. Below, we share our most important learnings.

1. The token management challenge

In the old MOBI.E system, tokens automatically had access to the entire network through the centralised platform. When a CPO migrates their infrastructure away from MOBI.E, those tokens need to be reconfigured to work under standard roaming arrangements.

'But here's the complication. Not every operator will migrate simultaneously.'

But here's the complication. Not every operator will migrate simultaneously. During the transition period, some infrastructure will remain on the MOBI.E platform, while other infrastructure operates under the new model.

For operators like EDP who want to maintain service continuity for their customers, this means implementing a dual-mode system. Their tokens need to work on both old-model chargers (still connected to MOBI.E) and new-model chargers (operating under the new RJME market model).

This requires sophisticated routing logic in the back-end systems. The CPMS must determine which authorisation path to follow based on the specific charger being accessed.

We've developed a migration approach that maintains this continuity. We keep tokens operational across both models throughout the transition. As each batch of chargers moves to the new framework, the back-end systems automatically adjust their authorisation routing. This happens without requiring any changes from drivers or partner eMSPs. This prevents the ‘big bang’ migration risk, where attempting to switch everything at once could potentially be a recipe for widespread service disruption.

Key takeaway for CPOs: Any operator managing a similar transition should ensure their back-end platform can handle dual-mode authorisation logic. The ability to route tokens intelligently based on infrastructure status isn't just a technical nicety—it's essential for maintaining service continuity.

2. The migration sequencing challenge

You can't flip an entire network overnight. Chargers need to be migrated, tested, and validated before moving to the next batch. But during this process, every stakeholder needs to know which infrastructure is on which model.

EMSPs need to understand whether they can access newly migrated chargers through standard roaming or still need MOBI.E integration. Drivers need seamless access regardless of technical changes happening in the background.

The phased approach also allows operators to identify and resolve issues with smaller batches before they affect the broader network. This essentially derisks the transition through controlled rollout rather than hoping everything works perfectly on day one.

Key takeaway for CPOs: Phased migration is about stakeholder communication, even more so than technical risk management. Every partner needs visibility into which infrastructure operates under which model, and when changes will occur.

3. The technical implementation challenge

The MOBI.E system had its own set of technical specifications and data requirements that created complexity for back-end operations.

For instance, it required additional metadata in Charge Detail Records (CDRs) to facilitate DSO invoicing, such as information about the connection point identifier (=CPE, which identifies the charger's connection point to the grid), voltage levels, and other grid-specific data. EV charging software built to support MOBI.E operations included custom extensions and special handling for these requirements.

Even seemingly minor technical details added layers of complexity. MOBI.E's legacy system used a decimal format for chip ID communication in certain scenarios. Modern charging infrastructure standardised on a hexadecimal little-endian format. Charge point management systems needed conversion mechanisms to handle this inconsistency. This is the kind of technical debt that accumulates when supporting unique market requirements over time.

As we manage EDP's transition, we're carefully deprecating these MOBI.E-specific features. At the same time, we're building out standard European capabilities. All whilst maintaining operational stability. The goal is to remove old functionality, but the biggest goal is to ensure that the deprecation happens in a controlled way that doesn't break existing operations during the transition period.

Key takeaway for CPOs: Your real challenge is: How to migrate your legacy systems without breaking existing operations? This requires charge point management software designed for graceful deprecation, not just feature addition.

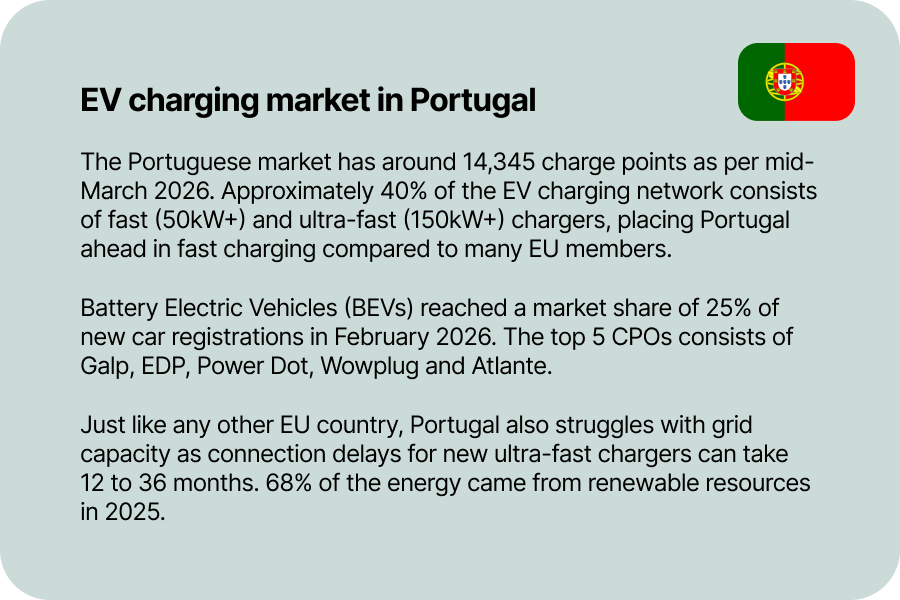

Figure 2: Portuguese EV charging market in April 2026. (Sources: Mobie.pt | EVInfrastructureNews.com | TheICCT.org | Mobie.pt | Alternative-Fuels-Observatory.ec.europa.eu)

Implications for charge point operators

Be aware that this transition matters beyond Portugal's borders. Let’s see what it means for different kinds of CPOs.

For Portuguese CPOs

The immediate concern for Portugal-based CPOs is execution. You need to:

- Plan your migration timeline.

- Assess what changes are required in your charge point migration system (or work with your platform provider to ensure they're managing this).

- Decide your approach to token management during the transition.

- Communicate clearly with your eMSP partners about the changes.

The 31 December 2026 deadline gives you time. But realistically, waiting until late 2026 creates unnecessary risk. Early movers can test their approach, identify issues, and refine their process whilst still having options if something doesn't work as planned. Being amongst the first to complete the transition also positions you as a technically capable operator in a market that's increasingly competitive.

You also get the opportunity to reclaim your energy margin. In the old model, eMSPs controlled energy procurement and pricing. In the new model, CPOs can choose to sell energy directly to drivers. This fundamentally changes the revenue model and allows for more direct control over pricing strategy.

For European CPOs considering Portuguese expansion

This transition simplifies market entry as the old MOBI.E model presented a barrier. Not insurmountable, but requiring specific integration work that differed from your operations elsewhere.

Post-transition, Portugal operates like most other European markets:

- Standard OCPI (Open Charge Point Interface) implementations.

- Familiar roaming arrangements.

- Conventional energy economics.

The distinctiveness that previously required special consideration is being removed.

If you've been evaluating Portuguese market entry but hesitated due to the unique technical requirements, the post-transition environment removes that friction. Portugal's growing EV adoption—25% BEV market share in February 2026—and government commitment to allocating €17.6 million for the purchase of electric vehicles and charging stations make it an increasingly attractive market for expansion.

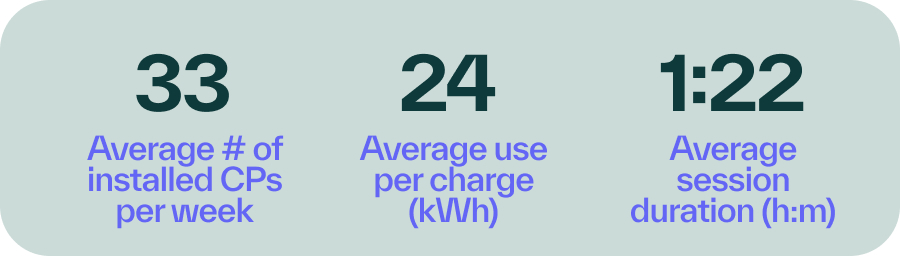

Figure 3: Average charging time per session, average kWh per session and number of new charge points per week in Portugal (as of March 2026). (Source: Mobie.pt)

The broader context of the Portuguese charging transition

Portugal isn't alone in experimenting with different charging market structures. Markets across Europe have implemented variations in how CPOs, eMSPs, DSOs, and regulatory bodies interact.

Portugal's bring-your-own-power model was particularly unusual in its execution. But the broader lesson is that operational flexibility matters. As EV adoption accelerates and infrastructure deployments scale, we'll likely see continued regulatory evolution across European markets.

Portugal's experience highlights an important reality. Market models can change. Regulatory frameworks evolve, sometimes requiring significant operational adaptations.

The Portuguese transition is happening over 18 months with clear deadlines and structured guidance. But future regulatory changes in other markets might not be so well-telegraphed.

The operators best positioned for success will be those who can adapt to these changes efficiently. They'll maintain service continuity through transitions. And they'll work with technology partners who bring deep market knowledge alongside technical capability.

You need partners who've navigated these transitions before and understand both the technical requirements and the broader market context.

The future of EV charging in Portugal

As of early 2026, no Portuguese CPO has yet completed a full migration away from the MOBI.E model. The regulatory framework only entered force in August 2025, and operators are still planning their approaches.

Over the coming year, we'll see how this transition unfolds in practice. Which operators move quickly? What challenges emerge that weren't anticipated in the planning phase? How does the market adapt to its new structure?

‘The underlying challenge—managing technical complexity whilst maintaining operational reliability—is something we encounter frequently as markets mature and regulations evolve.’

At GreenFlux, we're working closely with EDP through this process. We're applying our experience from managing complex backend operations across multiple European markets.

The Portuguese transition is distinctive in its specifics. But the underlying challenge—managing technical complexity whilst maintaining operational reliability—is something we encounter frequently as markets mature and regulations evolve.

For CPOs navigating this transition, the key is to start early, plan thoroughly, and work with partners who genuinely understand both the technical requirements and the broader market context.

Are you ready to make the transition to RJME? We’re happy to help with any questions you may have!